he week ahead could very well be the most important week of the month. Four central banks from the high income countries meet, the latest purchasing managers surveys will be released and the latest reading on the US labor market will be announced.

At the same time, Russia's move on Crimea and the US and European response may eclipse, at least partially, the economic focus of investors. Lithuania and Latvia have invoked Article 4, which requires consultation over Russia's actions when a member feels its security or independence is threatened. It is only the fourth such action in NATO history.

1. Ukraine (Moderate risk): Neither the US nor Europe are inclined to try to use military force to push Russia out of Crimea. There may be a short-lived wobble to the detriment of risk assets and beneficial for the dollar, yen and Swiss franc. Yet, the impact of geopolitics tends to be transitory. The early July G8 Summit in Sochi may be in jeopardy, but the G7/G8 had already been reduced to a caucus within the G20 and Russia's special role had already been diluted. Dis-inviting Russia from the G8 on grounds of not going to the UN for authority is laughable, given what happened in Iraq, but it does not mean it can't happen.

After Ukraine, Germany may have the most to lose from Russian actions. Its energy program and efforts to de-nuclearize seems to force greater reliance on Russian energy. The Soviet invasion of Afghanistan spurred an increase in military spending (which in the US began under Carter, not Reagan as often suggested). Many countries in the West are reducing military spending presently. There is some risk that China will use the West's distraction to press is case in the South or East China Sea. There may also be knock-on effect in the EU parliamentary election in May, where the anti-EU parties seemed to have moved into ascendancy.

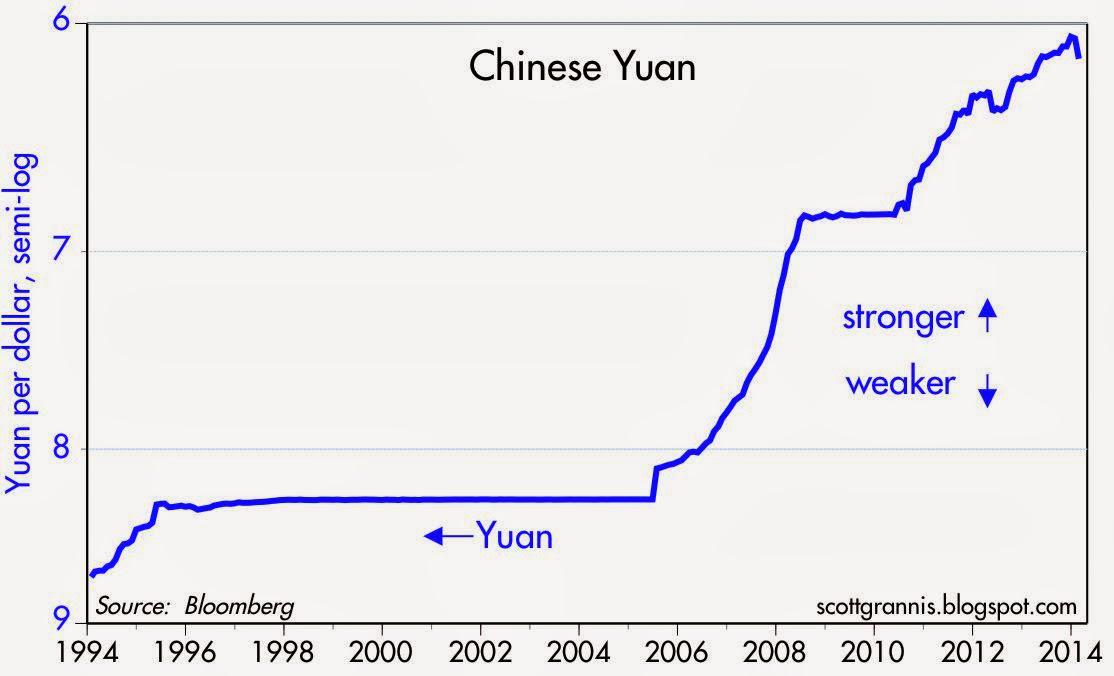

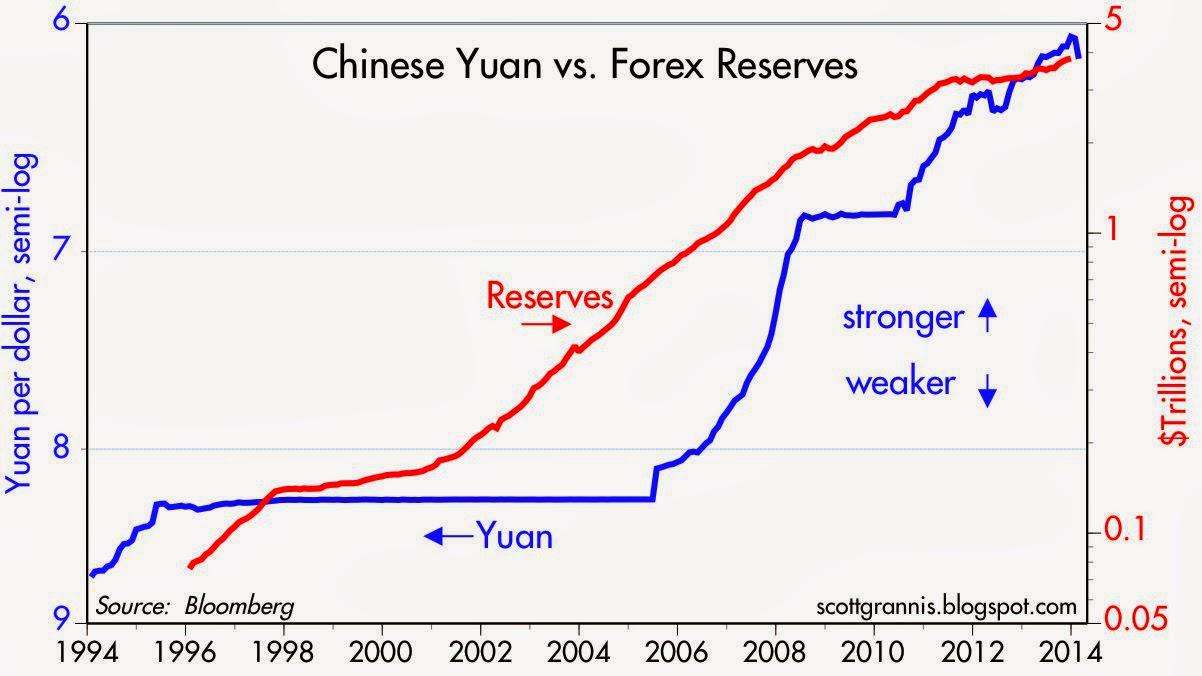

2. China (Low risk): China reported its official manufacturing PMI eased to 50.2 from 50.5 in January. The Bloomberg consensus was for 50.1. Output and orders slipped, while exports remained below the 50 boom/bust level for the third consecutive month. The PMI for large businesses eased to 50.7 from 51.4, while the reading for small businesses is contracting, as the HSBC flash PMI showed. The final manufacturing read and its service PMI, along with the official one, will be released first thing Monday in Beijing. In part, what is happening is a decline in investment, especially in the credit sensitive sectors, like infrastructure and real estate where investment has been excessive.

We expect the RMB to stabilize in the week ahead, though last week's decline did not prevent the Shanghai Composite from finishing the week with a three-day rally or the MSCI Emerging Market equity index from ending February at its highest level since January 23. The depreciation of the RMB is too small, given the relatively low-value added being done by Chinese workers, too boost exports and therefore the direct impact on trade is likely minimal at best. The National People's Congress begins at midweek and a solidification of the reform agenda should expected.

3. The Reserve Bank of Australia (Low risk): The RBA meets and the result will be announced Tuesday morning in Sydney. At its last meeting, it indicated that a period of rate stability is best and although the labor market continues to deteriorate and activity outside mining is not picking up sufficiently quickly, it is too soon to expect much of a change in the RBA's stance. The market may decide to ease for it by taking the currency lower. Technically, the February rally looks over and a new push lower appears to have begun. Its failure to resurface above $0.9000 signals initial downside risk back into the $0.8840-80 range.

4. Bank of Canada (Low risk): The Bank of Canada meets Wednesday, March 5. There is little to no chance of a rate cut and the BoC has already shifted its rhetoric to a more dovish/neutral tone since Carney went to the Bank of England. As in the US, the extent of the weather-induced economic disruption is not immediately clear and reasonable people can and do disagree. The February IVEY (Thursday) and jobs data (Friday), the latter to overshadow the January trade figures due out at the same time, may be more important for the Canadian dollar direction.

5. Bank of England (Low risk): Under Carney, the emphasis at the BOE is on using forward guidance to push against market fears of a rate hike sooner than the first part of next year. There is practically no chance of a change in rate. And because the BOE does not say anything when it does not do anything, there is no statement-risk as there is with the other central banks. The three PMIs (construction, manufacturing and service) are expected to show that UK economic activity has leveled off a bit at a reasonably robust pace.

6. European Central Bank (High risk): Of the central bank meetings this week, the ECB's is the only live one in the sense of a realistic possibility of a change. The failure to act in a substantive way could see the euro appreciate. Many, if not most, have focused on what we would regard as a symbolic 10-15 bp cut in the main repo rate. We suspect the euro could rally on this, as it is not the significant rate. It would unlikely even impact forward pricing. With the PMI likely showing continued expansion for the region and the preliminary CPI reading unchanged, officials will not feel compelled to take drastic measures such as adopting a negative deposit rate or launching a sovereign bond purchase program.

There has been some speculation that to boost the excess liquidity to keep EONIA (the key rate) stable and low, the ECB could formally stop sterilizing the SMP purchases. We suspect this would be a very controversial decision. Recall two German ECB members, Weber and Stark, resigned over the program. In the absence of sterilization, this would leave the SMP too close to QE, given the treaty prohibitions. We have advocated cutting the lending rate, which is the top of the official rate corridor and now sits at 75 bp. It is true the cap on EONIA. The ECB is also expected to use the new staff forecasts, that will project out to 2016 for the first time, to point to its belief that the low inflation may persist but the risk of outright deflation for the monetary union is slim. The euro could rally on this because it would strengthen the view that there is no appetite for those drastic measures.

7. US data (High risk): The US jobs data, with the February assessment due on Friday, March 7, tends to be among the most important economic reports of the monthly cycle. Yet, almost regardless of the report, whose thunder is partly stolen by the ADP estimate a couple days earlier, or the week's other data, which includes auto sales, purchasing managers surveys, the Fed's measured tapering pace is unlikely to be disrupted.

The Fed's tapering has not pushed up US 10-year yields this year, which have fallen by 38 bp through the end of February. Nor has it lent the dollar support, which has fallen against all the major currencies and many emerging market currencies (including Indonesian rupiah, Polish zloty, Hungarian forint, South African rand, Mexican peso, Brazilian real and Turkish lira).

Most of the US economic data in recent weeks have been reported below expectations. It means that the market has not fully grasped the magnitude of the slowdown being experienced here in Q1. Few really claim that it is only due to the weather, which has become a bit of a straw man in the blogosphere. We highlight three other forces at work: a) the inventory cycle, b) the end of the tax break for capex and c) the loss of income for 1.7 million Americans who had been collecting emergency jobless benefits. At the end of last week, there were a few secondary economic reports, notably new home sales, durable goods orders and Chicago PMI, were stronger than expected. With more important economic data out this week, it will be important to monitor this pattern, and if, better than expected data lends the dollar support. We suspect it may with a lag.

For the record, the Bloomberg consensus is for a 150k rise in February nonfarm payrolls. This is in line with the 3-month average of 154k, but below the 6-month average (177.5k), which is nearly identical with the 2-year average (179.6k). Although the consensus does not expect a decline in the 6.6% unemployment rate, we see the risk to the downside in response to the loss of the emergency jobless benefits. This is turn would reinforce expectations for a modification/evolution in the FOMC forward guidance at its March 18-19 meeting. Judging from the Fed funds and Eurodollar futures strips, the market is not pricing in the first rate hike until the second half of 2015.

Obama is expected to present the FY15 budget proposals on March 4. This tends not to be a market mover. Moreover, in recent years, due to the political paralysis, the Federal government has operated on the basis of continuing resolutions. Yet the budget proposal will help shape the coming debate. It takes place on the heels of news that FY13 budget deficit wasonly $680 billion from $1.1 trillion the previous year. The budget deficit fell to 4.1% of GDP from 6.8%. It is projected to continue trending lower over the next few years. Obama is expected to avoid further cuts in spending, drop efforts to use chain-weighted CPI measures to slow Social Security payouts and promote public investment.