Interesting Words

Abenomics refers to the economic policies advocated by Shinzō Abe since the December 2012 general election, which elected Abe to his second term as Prime Minister of Japan. Abenomics is based upon "three arrows" of fiscal stimulus, monetary easing and structural reforms.[1] The Economist characterized the program as a "mix of reflation, government spending and a growth strategy designed to jolt the economy out of suspended animation that has gripped it for more than two decades."

The term "Abenomics" is a portmanteau of Abe and economics, and follows previous politicalneologisms for economic policies linked to specific leaders, such as Reaganomics,Clintonomics and Rogernomics.

A portmanteau ( i/pɔrtˈmæntoʊ/, /ˌpɔrtmænˈtoʊ/; plural portmanteaux or portmanteaus) or portmanteau word is a combination of two (or more) words or morphemes, and their definitions, into one new word.[1][2] The word comes from the English portmanteau luggage (a piece of luggage with two compartments), itself derived from the French porter (to carry) and manteau (coat), which is a false friend of the French compound word porte-manteau meaning coat rack.

i/pɔrtˈmæntoʊ/, /ˌpɔrtmænˈtoʊ/; plural portmanteaux or portmanteaus) or portmanteau word is a combination of two (or more) words or morphemes, and their definitions, into one new word.[1][2] The word comes from the English portmanteau luggage (a piece of luggage with two compartments), itself derived from the French porter (to carry) and manteau (coat), which is a false friend of the French compound word porte-manteau meaning coat rack.

A portmanteau word fuses both the sounds and the meanings of its components, as in smog, coined by blending smoke and fog,[1][3] ormotel, from motor and hotel.[4] In linguistics, a portmanteau is defined as a single morph which represents two or moremorphemes

In linguistics, a morpheme is the smallest grammatical unit in a language. The field of study dedicated to morphemes is called morphology. A morpheme is not identical to a word, and the principal difference between the two is that a morphememay or may not stand alone, whereas a word, by definition, is freestanding. Every word comprises one or more morphemes.

Once the second biggest economy in the world and a fountainhead of innovation, the land of the rising sun has gradually slipped down the global rankings after a lost decade, losing out its placing to China. Will Abenomics offer the ray of light that will lead Japan out of the tunnel?

(click to enlarge)

Chart 1. Since 1990 asset bubble bust, the Nikkei 225 has yet to scale new heights (source: Yahoo Charts)

Declining Competitiveness

(click to enlarge)

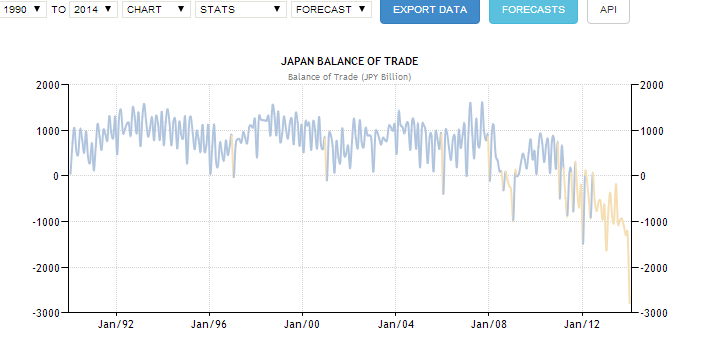

Chart 2. Japan's balance of trade has been on a downward spiral (sourcewww.tradingeconomics.com)

During the stagnant 90s, Japan's sole bright spot came from its trade surplus as the rest of the world demanded highly innovative Japanese goods. However, since then Japanese competitiveness has been declining in the face of the rising challenge from Korea and China as manufacturing powerhouses. Its once famous and solid trade surplus gave way to a trade deficit for the first time in 2007.

For example, Japan used to be number two in the car manufacturing industry (see 1999 production numbers) but in the most recent survey by OICA, Japan has dropped to number three, producing only slightly more cars than it did in 1999.

Table 1. Japan used to be the second largest producer of automobiles (source: OICA)

Table 2. Japan has dropped to third by 2012 (source OICA)

Economically struggling, politics not helping

While the economic engine face exogenous headwinds, domestic policies have not been given the stability needed for implementation and results. Since Prime Minister Koizumi's term ended in 2006, no Japanese premier has lasted more than one year in office.

Name

|

Term of office

|

Dates of birth

|

Tomiichi Murayama

|

1994-1996

|

3 March 1924 (age 89)

|

Yoshirō Mori

|

2000-2001

|

14 July 1937 (age 76)

|

Junichiro Koizumi

|

2001-2006

|

8 January 1942 (age 72)

|

Yasuo Fukuda

|

2007-2008

|

16 July 1936 (age 77)

|

Taro Aso

|

2008-2009

|

20 September 1940 (age 73)

|

Yukio Hatoyama

|

2009-2010

|

11 February 1947 (age 67)

|

Naoto Kan

|

2010-2011

|

10 October 1946 (age 67)

|

Yoshihiko Noda

|

2011-2012

|

20 May 1957 (age 56)

|

Table 3. Source: Wikipedia, No minister has lasted more than one year in office since the charismatic Junichiro Koizuimi stepped down in 2006

Prime Minister Shinzo Abe was sworn in late 2012 and has become the first premier to last more than one year in office. This has provided the rare political stability for the implementation of public and fiscal policy and his plan nicknamed "Abenomics".

The Three Arrows of Abenomics

Since Prime Minister Shinzo Abe took office in December 2012, he has embarked on a three point plan to revive Japan. His three arrows included a massive fiscal stimulus to increase spending by 2 per cent of GDP, monetary easing to reach a 2 per inflation target and structural reforms to improve Japan's competitiveness.

(click to enlarge)

Chart 3. The First Arrow: government spending has increased but at a slower pace after 2012 (source:www.tradingeconomics.com)

(click to enlarge)

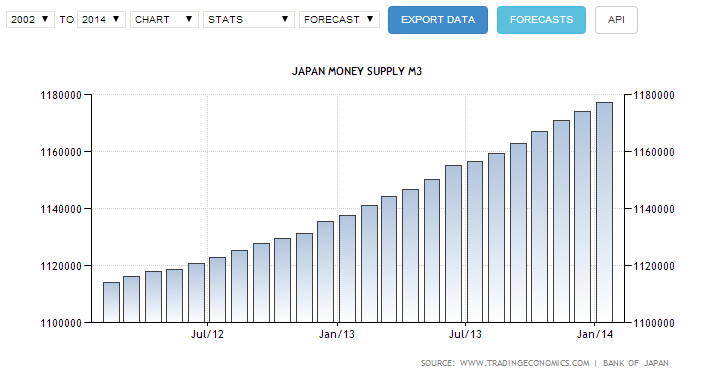

Chart 4. The Second Arrow monetary expansion has driven M3 to a record in 2014 (source: www.tradingeconomics.com)

Has Abenomics Worked?

However, the implications of the first two arrows has been a weakening of the Yen currency (JPY). In the past a weak JPY boosted the trade balance by cheapening exports and making imports dearer. However in modern times, more Japanese production has gone offshore and with increasing reliance on energy imports to make up for the loss of nuclear energy post-Fukushima, the weakened JPY has led to worsening of the balance of trade.

(click to enlarge)

Chart 5. Figure JPY has weakened by 25% vs the USD from 80 to 100 since 2012 (source: Yahoo charts)

(click to enlarge)

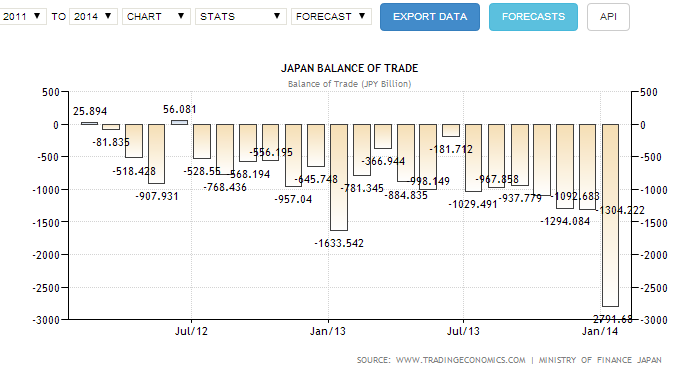

Chart 6 Trade deficit has worsened under the Abenomics policy (source:www.tradingeconomics.com)

In other words, the deteriorating trade balance is making GDP growth weaker than where it should have been. More than ever, internal restructuring (the third arrow of Abenomics) is needed to invigorate productivity and sharpen competitiveness. Areas to look at include agricultural reform (see here for a more detailed report on the problems facing Japanese agriculture) and revising the energy policy to re-examine its nuclear policy. Unlike the first two arrows, internal restructuring is more of a long term fix to competitiveness and any short term improvement in the trade balance is unlikely.

Growing from within

With external demand subtracting from GDP growth in the short term, Japan's economy is increasingly reliant on domestic demand in the form of consumption, government expenditure and private investment to drive growth. Consumer spending at JPY 315 trillion makes up 60 % of Japan's JPY 526 trillion economy and has been growing steadily since 2012

(click to enlarge)

Chart 9. Consumer spending has been on a steady rise since 2012 (source:www.tradingeconomics.com)

Despite a growing consumer, GDP growth has been slowing of late as seen in the below forecast figures for the recent quarters, dragged down largely by external demand in the form of the trade deficit.

(click to enlarge)

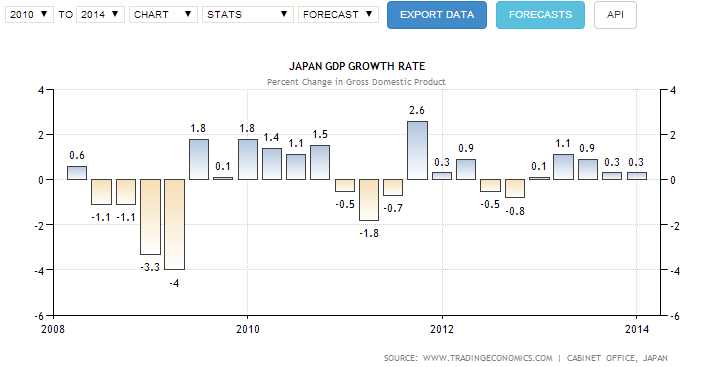

Chart 8 After the initial Abenomics-induced surge, GDP growth has slowed (source:www.tradingeconomics.com)

With the Japanese consumer facing uncertainty going forward with the increase in sales tax in April to 8% from the current 5%, things do not bode well for the economy in 2014 unless more drastic policy actions are taken.

Conclusion and the challenge ahead

The jury is still out on the success of Abenomics. The first two arrows of increased fiscal spending and monetary expansion have not boosted Japanese competitiveness in the international trade market as much. The third arrow of domestic restructuring still requires time before the impact can be felt. Until then the whale will have to rely on the domestic spending (the consumer, the government and business investment) to drive growth. With the impending rise in sales tax, it remains to be seen if the consumer which forms the bulk of the economy will drive the whale through turbulent seas.

Investment Thesis

From an investment viewpoint, ProShares Ultrashort MSCI Japan ETF looks to be a suitable instrument to gain a short exposure to Japan until the impact of the consumer tax rise is fully reflected in the expected negative GDP growth in the second quarter. Investors with long exposure to the Japan via the ETFs iShares MSCI Jan ETF and ProShares Ultra MSCI Japan ETF may consider trimming the exposure until after further clarity emerges on the government's plans to improve Japanese competitiveness.

Comments (1)

- CautiousInvestorComments (2912)When you look at the above chart highlighting Jpan's GDP, it's quite evident that growth in GDP is faltering as the effects of the massive increase fiscal spending wane. Abe was quite eagier to shoot the first two arrows, fiscal spending and additional QE as these are "fun" and politically popular. Even without the third arrow of sturctural reform, they were supposed to expand exports, increase profits and increase wages. But, while corporate profits have increased in part because of a lower currency, exports in real terms have remained stagnant while imports of fossil fuels have increased to replace lost nuclear power, leading to a wider trade imbalance. Further, real consumer incomes have fallen to a sixteen year low becaue profits are not being shared because much of Japan's manufacturing has been moved offshore. Abe, predictably, is dithering on structural reform because of political opposition but if he fails in increasing female labour force participation, consolidating farms, breaking down labour market divisions and raising competition in healthcare – which are sensible and feasible - then Abenomics will go down in history as a failure and Japan will relapse into an economic coma.